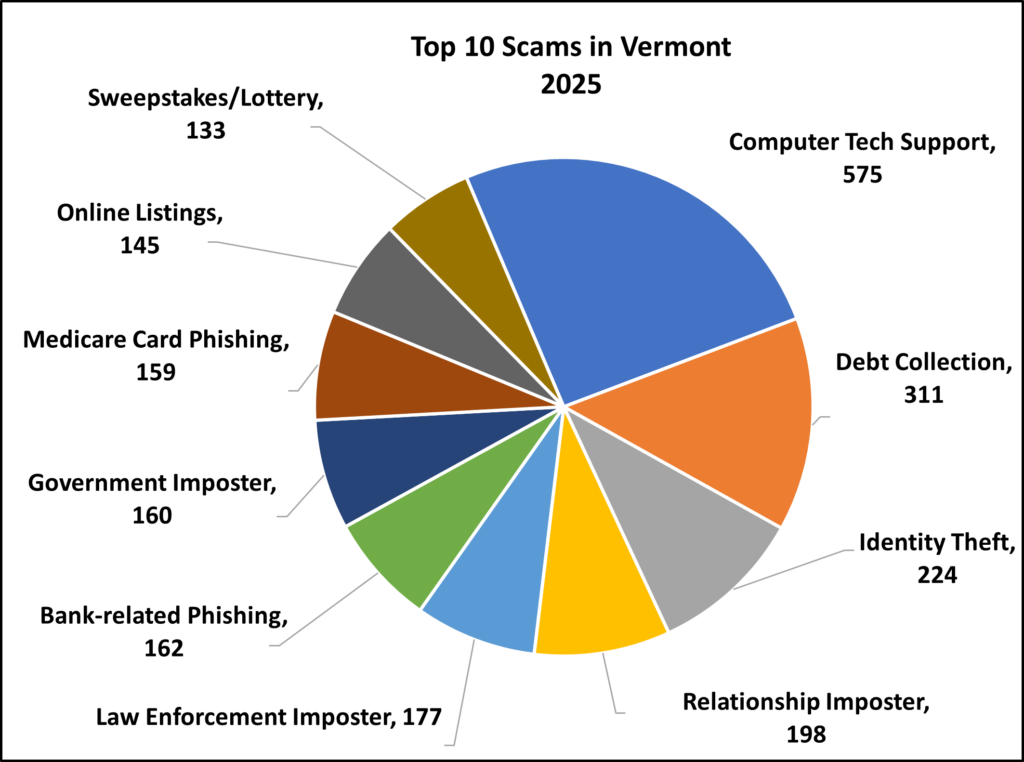

Vermonters made a total of 3,982 scam reports to the Attorney General’s Consumer Assistance Program (CAP) in 2025 – an increase of 12% over the previous year. Leading the list for the fifth consecutive year was the “Computer Tech Support” scam, totaling more than a quarter of the top scams reported. This scam tricks people with sudden alerts about alleged computer issues, such as expiring antivirus software or malware infections. Debt collection scams also rose in 2025, appearing in the top ten list for the first time and ranking second overall.

Another new scam in the top ten list this year is the government imposter scam – a variation on any other imposter scam where the scammer poses as a government agency requesting money or personal information. A recent example of this scam is the Supplemental Nutrition Assistance Program (SNAP), known in Vermont as 3SquaresVT, recipient scam, which spiked in November and again just last week. In this scam, scammers posing as a government entity sent text messages and called SNAP recipients, warning them that their food and nutrition benefits have been stopped until they provide personal information to verify their eligibility.

“Educating Vermonters is the best way to protect them from scams,” said Attorney General Charity Clark. “If you receive unsolicited calls, emails, or text messages – especially those threatening legal action – do not respond. Slow down and talk with a trusted family member, friend, or call my office’s Consumer Assistance Program for help.”

More information about scam prevention strategies and other resources can be found on the CAP Connection blog, on Attorney General Clark’s social media sites, and by signing up for the VT Scam Alert System. To sign up, visit CAP’s scam prevention website. Roughly 11,000 Vermonters have already signed up to receive alerts.

The VT Scam Alert System was previously established through a partnership with Vermont Emergency Management that granted the Attorney General’s Office the ability to issue alerts utilizing limited features of the VT-ALERT system. VT-ALERT is the state’s notification system for emergencies, severe weather, roadway interruptions and hazards, environmental hazards, and more. Whenever someone signs up for VT-ALERT, they have the ability to opt into notifications about scams among the list of options. VT-ALERT’s existing users can also update their preferences to add scam alerts.

Attorney General Clark reminds Vermonters to report scams and get support if you or a loved one falls victim to a scam by contacting her Consumer Assistance Program. Call 800-649-2424 or email AGO.CAP@vermont.gov.

The Top 10 Scams of 2025:

| RANK | Top 10 Scams 2025 | # Reported |

| 1 | Computer Tech Support | 575 |

| 2 | Debt Collection | 311 |

| 3 | Identity Theft | 224 |

| 4 | Relationship Imposter | 198 |

| 5 | Law Enforcement Imposter | 177 |

| 6 | Bank-related Phishing | 162 |

| 7 | Government Imposter | 160 |

| 8 | Medicare Card Phishing | 159 |

| 9 | Online Listings | 145 |

| 10 | Sweepstakes/Lottery | 133 |

Total Reports in the Top 10 in 2025: 2246

Total Number of All Scams Reported to CAP in 2025: 3982

A chart containing the Top 10 Scams of 2025 is available on the Attorney General’s website along with a complete overview of the Top 10 Scams of 2025, including how to spot them.

Top 10 Scams of 2025 Overview

The scam: You receive a phone call, pop-up, email or text message on your computer claiming to be a well-known company; sometimes it’s a tech company like Norton, Apple, or Microsoft, or it’s Amazon saying your credit card has been charged, or there is a package delivery delay. They will urge you to contact them due to a problem: your electronic device has a virus, your device security subscription has been automatically renewed, or you have been charged for services you did not receive or request. You may be prompted to click a link or call a number to contact. They will try to persuade you to give remote access to your device to fix the problem and sometimes will even ask for immediate payment for their services or have you login to your online bank account to initiate a transfer.

How to spot the scam: Companies will not call with tech support unless you request that they contact you. Legitimate tech support companies do not display communications to their customers as random notices or alerts on your device. Tech support will not call you to warn you about security incidents, that your account has been renewed for a subscription you do not recognize and will not send you random links with instructions for you to click on URLs. If you receive a package that you do not recall ordering, check your statement history to see if you have been charged. Packages without a return address are highly suspicious.

What to do: When contacted about a supposed business relationship, take steps to verify, especially if you do not remember purchasing the products/services. Never click on links or provide remote access to your computer from an unknown sender or pop-up message on your device’s screen. If you receive a pop-up message you cannot click out of, shut down, restart, or unplug your device. If you get a call from “tech support”, hang up. Also, be careful when searching for tech support online. Some users have been scammed by calling inaccurate phone numbers listed online. If you are concerned about charges made to your accounts, log in to your account directly and contact your financial institution. If you receive a package that you did not order, write “return to sender” on it and give it back to the mail carrier.

- Debt Collection

The scam: Scammers pose as debt collectors and require immediate payment. They may claim to be familiar businesses, such as a toll operator, or utility company and threaten unsettling consequences like fines, electricity shutoff, or legal action.

How to spot the scam: Collectors are not allowed to threaten you with arrest over debts owed. You can request verification of the debt, which must be sent to you in writing. If you ask them to stop contacting you, they are generally required to stop.

What to do: Disengage. Hang up the phone. Don’t reply to text messages asking for payment or redirecting you to a link. If you think you do actually owe money to an entity of a debt collector, make sure to use trusted contact information when communicating with them. There are consumer protections for the collection of debt. Scam collectors do not usually adhere to debt collection regulations.

The scam: Your personal information is compromised and may be used for another’s financial gain. This can look like: an unauthorized charge on an account, receiving a letter about a new account opening or a data breach notification. You might stop receiving legitimate bills and other mail or start to get bills for products and services that you didn’t arrange. Accounts you are not familiar with may be listed on your credit report.

How to spot the scam: Beware of communications denoting unexpected bank transactions, credit card or benefit applications. If your expected bills are not showing up, or you are receiving correspondence in someone else’s name, report it.

What to do: Don’t give out personal information, such as your Social Security number, passwords, personal identification numbers, and financial accounts. Review your credit reports at least once a year. (You can access your credit report for free). Carefully check bank account statements and benefits to verify transactions. Shred documents and expired credit cards before you throw them out. Verify security breach notification letters received on the Attorney General’s website. If your information has been stolen by an identity thief, take identity theft protection steps. You can safeguard your financial information by placing a credit freeze on your credit report.

The scam: Scammers pose to be someone you trust and pretend to be in a crisis to convince you to send them money. They may also ask you for a favor. These scammers pose as grandchildren, friends, relatives, budding romantic partners, and other close contacts. Scammers impersonate people you adore and play on your fears to have you send money urgently. After the initial contact, you may be redirected to a lawyer or parole officer. Sometimes the voices in the phone call sound like relatives due to scammers utilizing artificial intelligence. In-person couriers may also come to retrieve funds.

How to spot the scam: Contacts come in as calls, emails, or online messages. Sometimes it’s someone you haven’t heard from in a while. They require urgency and ask for secrecy. You may be instructed not to speak to your loved one on the phone. For new relationships, they have excuses as to why they can never meet in person, they won’t video chat with you when you would like, they have a pressing need for financial help (at any point in the relationship).

What to do: Take steps to verify. Check out if they really are who they say, even if they sound like a loved one. Artificial intelligence (A.I.) makes it easy for scammers to copy voices of people in your life. Slow down your response and contact someone you trust to verify if there is an emergency. You can also choose a code word or phrase to use with friends and family to verify the person is who they claim to be. If they don’t know the code, they are not your friend or family member. Do not give money to in-person couriers. For new online relationships, involve your inner circle as a sounding board. Use existing image search tools to find out more about the person, such as whether the profile is duplicated. Ask for candid, uncommon photos to be taken and sent in the moment and don’t trust fuzzy, or altered pictures.

- Law Enforcement Imposter

The scam: You receive a phone call unexpectedly, claiming to be a police officer, sheriff, U.S. Marshall, or similar. The caller will claim there is outstanding legal action. They may claim you have missed jury duty or there is a warrant for your arrest, for example. When you engage, urgent payment is demanded to make the problem go away. Payment does not solve the supposed problem, and they keep calling.

How to spot the scam: Law enforcers do not warn you ahead of time about a pending warrant or arrest. Legal action follows standard due process and there is a lot of paperwork, typically delivered by mail or served in person. For jury duty assignments, you first must be selected through a process called a jury draw that occurs at the courthouse.

What to do: Hang up on all arrest threats and report them. Watch out for similar government imposter scams that purport to be agents of government, including from the Social Security Administration, the IRS and more.

- Bank-related Phishing

The scam: You receive an email or phone call claiming to be from a financial institution or entity that keeps personally identifiable information (PII). The communication may claim that your account is in danger or has been suspended, or that your card is on hold due to suspicious activity. Emails may also include links to phony websites. Phone calls may claim that there has been fraudulent activity involving your account, and the scammers demand personal information about you and your account.

How to spot the scam: Scammers mask their actual identity by changing the sender’s name to the name of the cloned entity. Look at the email address before opening the email. You will often find an account not affiliated with the claimed entity. Similarly, scammers can spoof phone numbers of real businesses. If you answer a call that appears to be from a company with which you maintain an account and they ask for your personal and/or account information, hang up and call the company directly on a number you trust and verify their attempt to contact you.

What to do: Do not reply to the email or click on any links or attachments included on the message. If you receive a call, hang up the phone. Correspond with entities only using verified contact information, such as information listed on your statement.

- Government Imposter

The scam: Fraudsters pose as familiar state or federal government agencies to steal your money and personal information. They may claim to be the Department of Motor Vehicles (DMV), Economic Services Department, or Federal Trade Commission (FTC), and more. The scammers may threaten to revoke, pause, or suspend specific government benefits, if personal information or money is not provided. The scammers may recreate frequently searched government websites, such as that of the U.S. Passport office, and claim to render the same services.

How to spot the scam: Scammers impersonate government agencies because it creates a sense of authority and urgency. They hope to induce fear and panic, driving people to act quickly to resolve a pressing problem. However, government officials do not call and threaten benefits suspension in exchange for personal information or money.

What to do: Hang up on threatening calls that claim to impact your benefits. If a call or message seems legitimate, take steps to verify by contacting the government agency directly using official contact information. When seeking out government services online, always check that government website addresses end with “.gov”, and keep searching when they do not. Most federal agencies can be located on the USA.gov website and State of Vermont agencies can be found on the Vermont.gov website.

The scam: Scammers will call, often with a live call and from a spoofed caller ID number and pose as Medicare representatives to gain your personal information and money. These scams are most frequent during times of open enrollment but can occur year-round. The scammers will state they need your Medicare card number or Social Security number to keep your coverage active and verify medical information. The calls may also claim that coverage is expiring or in need of renewal. Scammers will also ask if you received a “new Medicare card.”

How to spot the scam: In general, Medicare cards do not expire. Unless you have called Medicare using the 800 number on the back of your card and requested a callback, Medicare will not call you. Medicare representatives will never call you to verify your information, sell you products, tell you that your coverage is expiring, or to issue you a new card.

What to do: Never provide your Medicare number or other personal information and payment to unknown callers. In Vermont, representatives of the State Health Insurance Assistance Program (SHIP) at 1-800-642-5119 through local Area Agencies on Aging can help address Medicare questions. Other questions and concerns about Medicare coverage can be directed to Medicare at 1-800-MEDICARE.

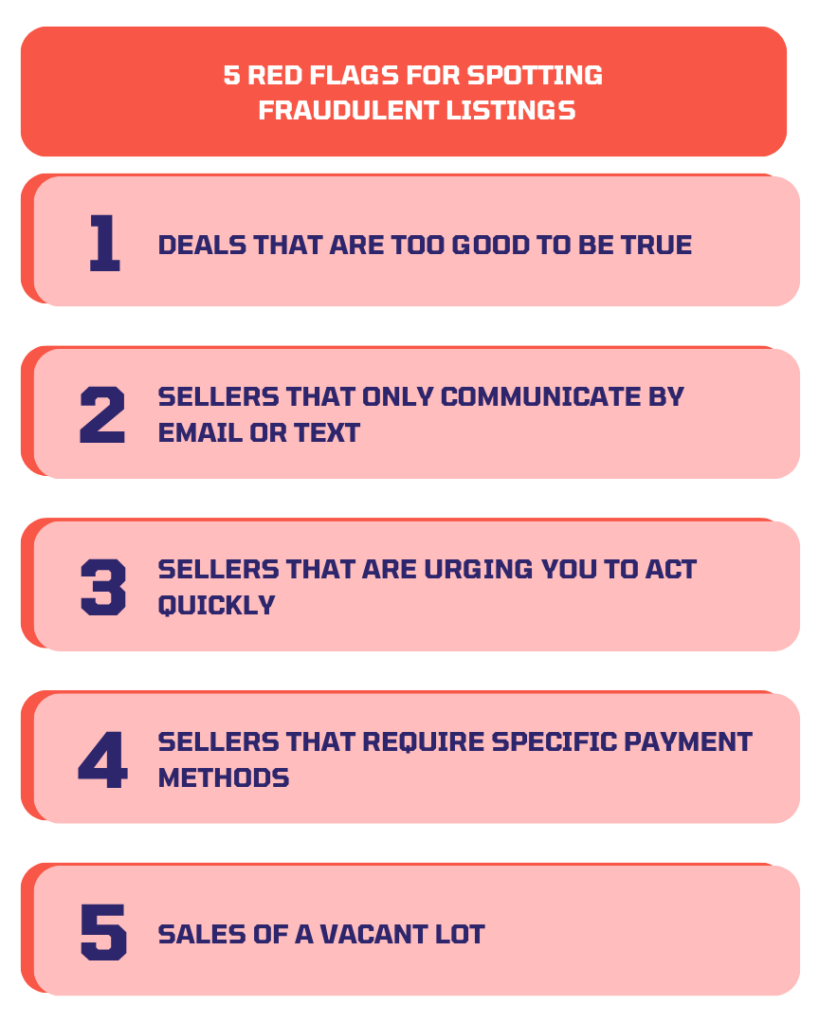

The scam: Fake websites or phony listings draw you into a purchase that is enticing. Listings may include online storefronts, Facebook Marketplace and Craigslist posts, cheap pet sales, and websites with steep discounts that don’t deliver after payment has been made. This scam can also appear in online rental listings as well as target online sellers.

How to spot the scam: Be skeptical of unrealistic offers. Watch out for requests for money in any form when not made in person. Scammers likely will not want to talk on the phone or meet in person. Heed warnings in user reviews and other online commentary.

What to do: Investigate the person/profile of the seller. If their profile is new and they have no friends and photos, they are likely a scam. Verify the website URL is the actual business’ site and not a copycat. Research new websites you are considering doing business with by looking up online reviews and business registrations, taking note of how long the company has been operating. Perform online searches of the business with “scam” and “complaints” to see if issues generate. For classified-type listings, complete your transactions in cash and preferably at a safe place in person.

The scam: You will be notified by phone, email, or mail that you won a prize or a quantity of money. In some cases, you will even receive a realistic-looking check – but it is fake! You are instructed to pay fees and give your financial and personal information to claim your prize. They often use a legitimate sweepstakes name, like Publishers Clearing House.

How to spot the scam: Legitimate sweepstakes and contest businesses, like Publishers Clearing House and Mega Millions lottery, are frequently impersonated. Know that legitimate sweepstakes/lotteries that you entered never require a payment or processing fee to release your prize.

What to do: If it sounds too good to be true, then it’s not true. You don’t need to pay fees to an entity, whether for processing, shipping/handling, insurance, and taxes, etc., or give your financial information to claim a prize.

Scams Reported by Businesses in 2025

Of the 3982 scams reported to the Consumer Assistance Program (CAP), 176 were submitted by Vermont businesses.

The 5 most common scams for businesses include: Imposters of business personnel, fake orders, business identity theft, phishing, and government imposters.

The top scam for businesses to look out for is the Imposter of Business Personnel aka Business Email Imposter scam:

In 2025, CAP received 54 reports from Vermont small businesses experiencing business imposters. Business owners and employees must be vigilant. This scam is particularly pervasive and can infiltrate business operations.

Scammers impersonate employees or familiar internal/external business representatives via email. They contact company bookkeepers and office administrators, asking them to redirect wire transfers, update direct deposit or bank account information, or to write checks. By impersonating an employee’s email address or creating a fake personal email for the employee, scammers can steal money from businesses and their employees’ paychecks.

Vermont businesses and non-profits should always verify email addresses and speak directly with an employee or business representative in person or via phone when sending money or changing financial information. Oftentimes, scammers will use an email address that only slightly varies from an employee’s true email. Sometimes, a business email system is hacked. Be wary of any email coming from outside your company’s domain. CAP urges business owners to educate their entire company on scams that target businesses and establish safeguards.

To learn more about how to protect your business from these scams, watch CAP’s Avoiding the Business Imposter Email Scam Video and visit the CAP Connections blog post on Vermont Business Imposter Email Scams Are on the Rise.

CAP further encourages businesses in Vermont to take the following steps to help prevent scams:

Train Your Employees: Your best defense is an informed workforce.

Verify Invoices and Payments: Check all invoices closely. Never pay unless you know the bill is for items that were actually ordered and delivered. Tell your staff to do the same.

Be Tech-Savvy: Don’t believe your caller ID. Imposters often fake caller ID information so you’ll be more likely to believe them when they claim to be a government agency or a vendor you trust.

Know Who You’re Dealing With: Never send money to parties you cannot verify. Check registration history, recommendations, and confirm contacts by calling. Before doing business with a new company, search the company’s name online with the term “scam” or “complaint.”

Businesses are encouraged to call CAP to report scams, ask questions, and get resources.