By Crystal Baldwin

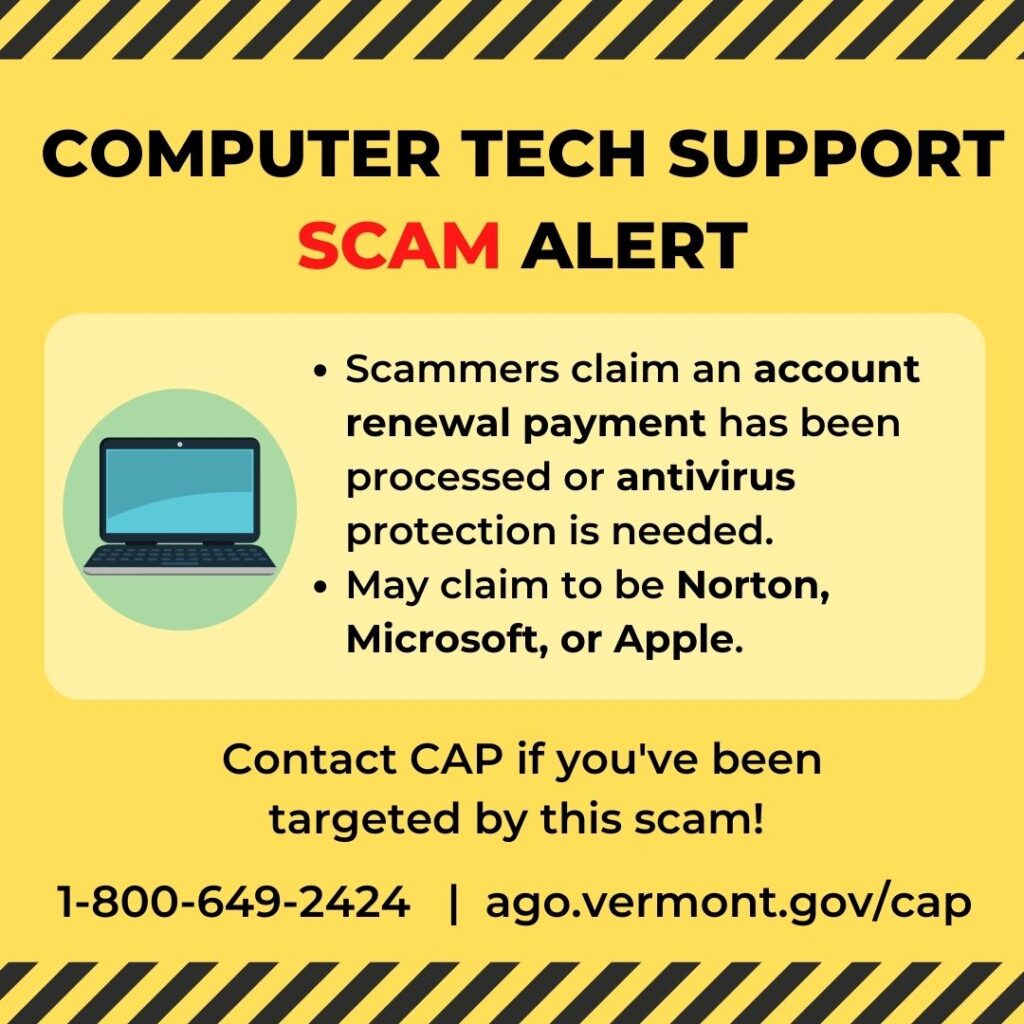

Computer tech support scammers are imposters that immediately gain trust by using well-known company names like Norton, Microsoft, or Apple, or by expressing a desire to help fix a daunting problem. Ranking third among the scams with the highest dollar loss, $695,240, in Vermont in 2021, this scam is historically successful due to its ability to establish a sense of familiarity and legitimacy garnered by the scammer’s suggested affiliation with a company and their technical prowess.

In the computer tech support scam, you are contacted by phone, pop-up or email on your computer. The message spikes your anxiety and drives your response to be reactive. Tech scammers may claim, “There is a virus on your device,” “Your security subscription has been automatically renewed,” or “You have been charged for a year’s subscription of antivirus.” In the communication, a link or phone number is included, which you are urged to contact immediately to rectify the issue.

While in reaction mode, you call, hoping to resolve the issue. During the call, the scammer will try to persuade you to give remote access to your device to fix the problem, and sometimes will ask for immediate payment for their services. In scenarios where a refund is requested, they facilitate what appears to be a transfer of funds by walking you through steps to log into your own online bank account. Utilizing their program and ability to freely roam on your computer while they have remote access, they disguise the origin of the funds transfer, which is in actuality a transfer of funds between your own bank accounts.

Tech support scammers further escalate the call, using high tones of voice, demands of urgency, and call on your empathy to help solve a problem they created. The scammer’s tactics pull the recipient of the scam further into reaction mode. While in reaction mode, responses are based on impulse and with little additional collective data. Once a person has more information, through the process of asking questions and seeking out resources, the ability to think critically and problem-solve the issue comes back online.

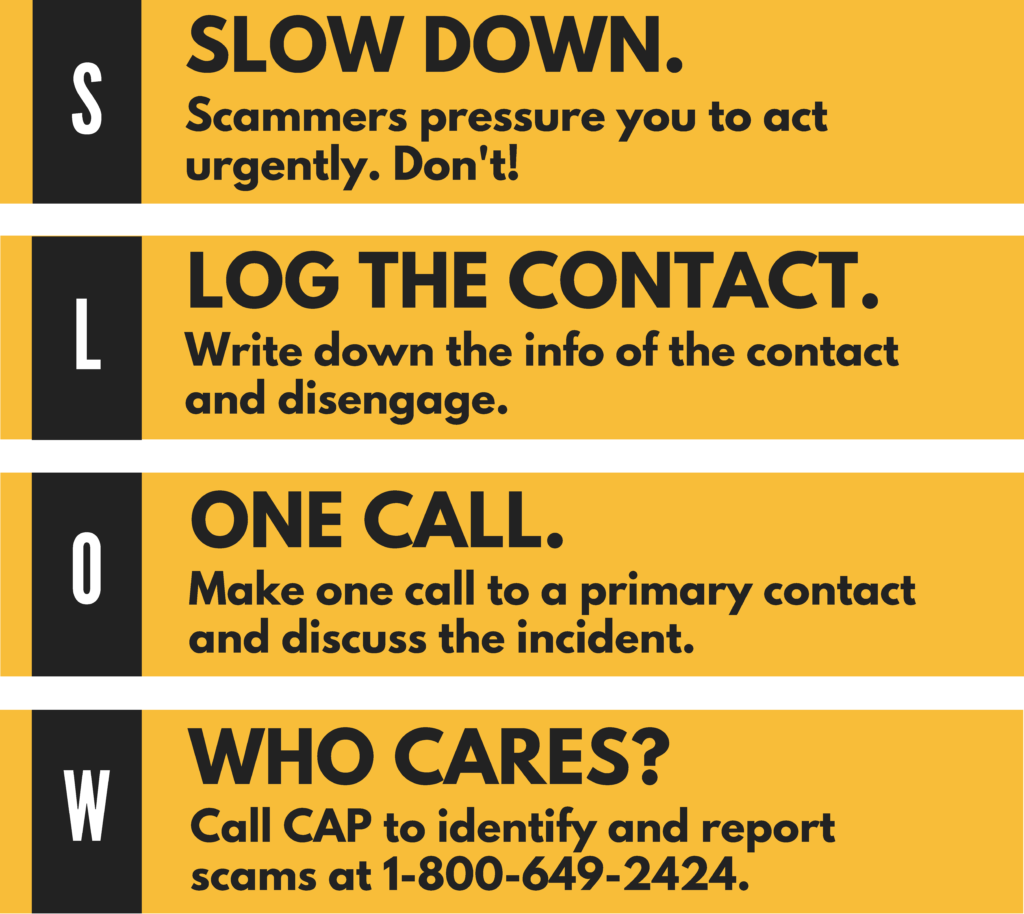

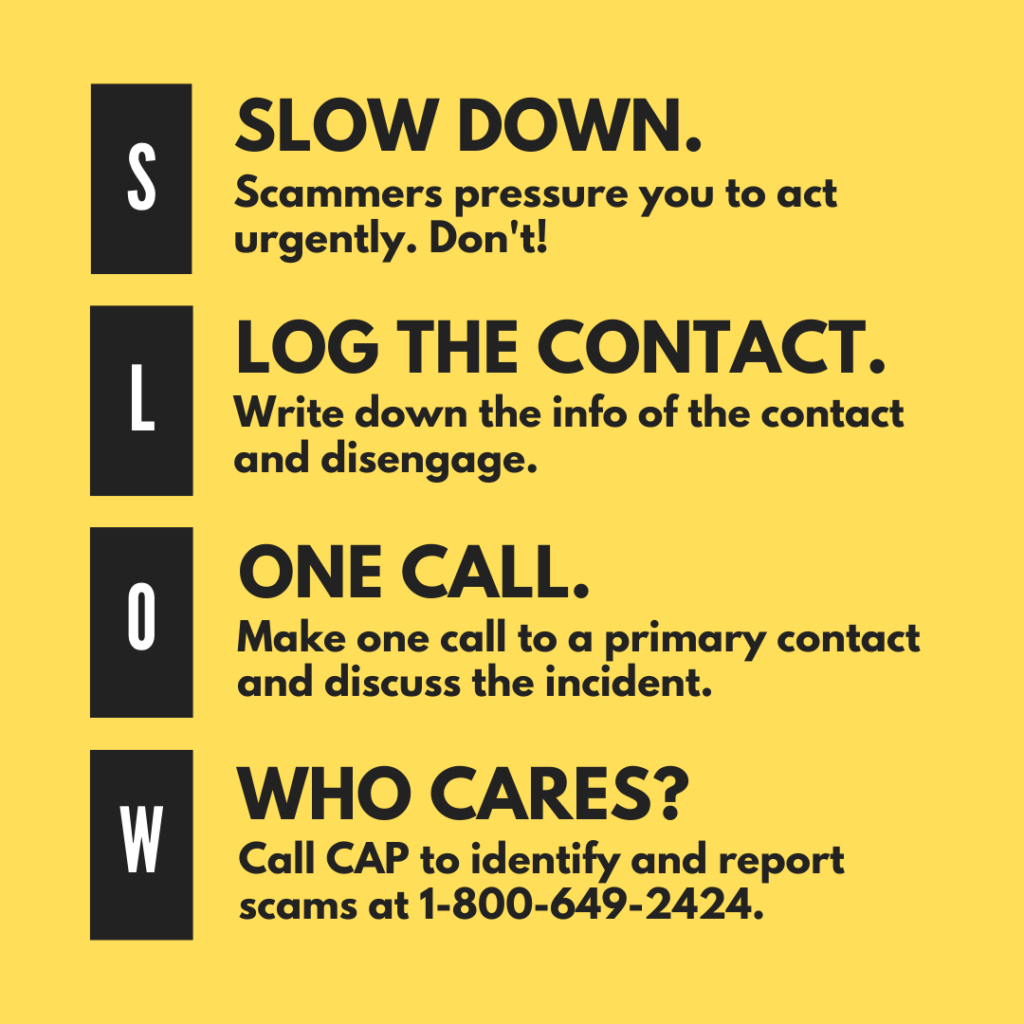

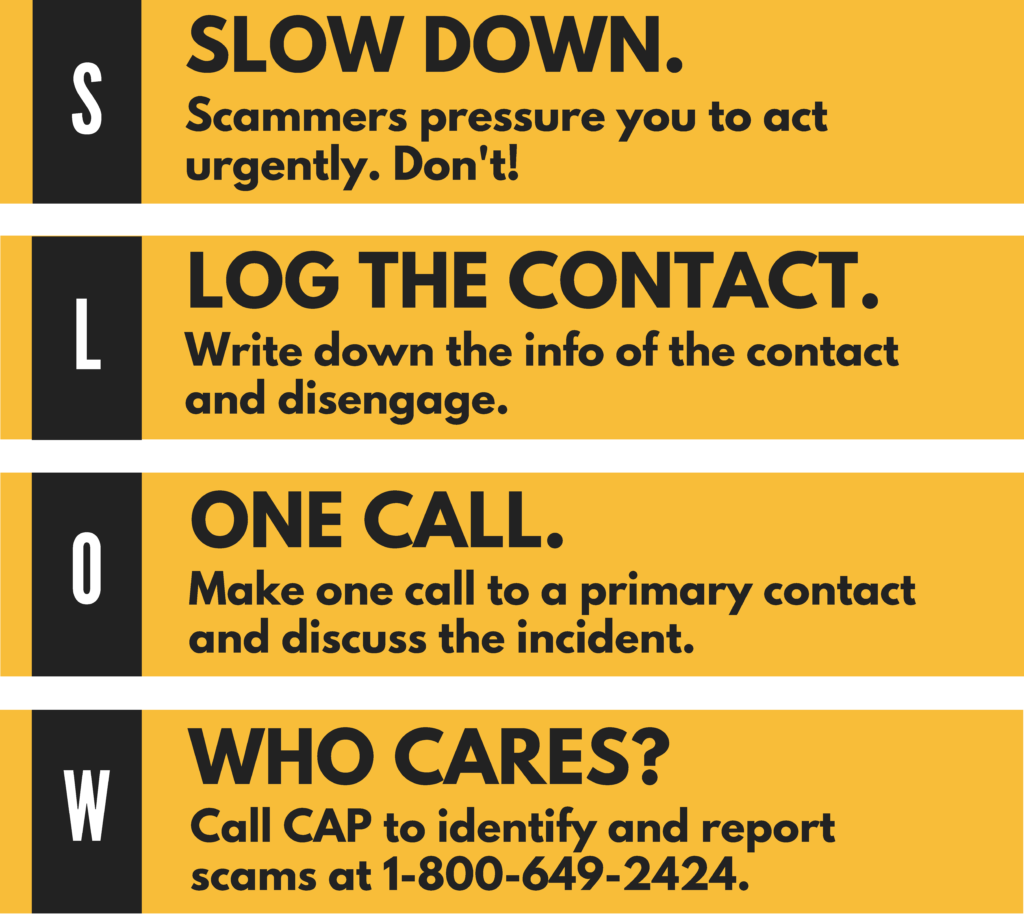

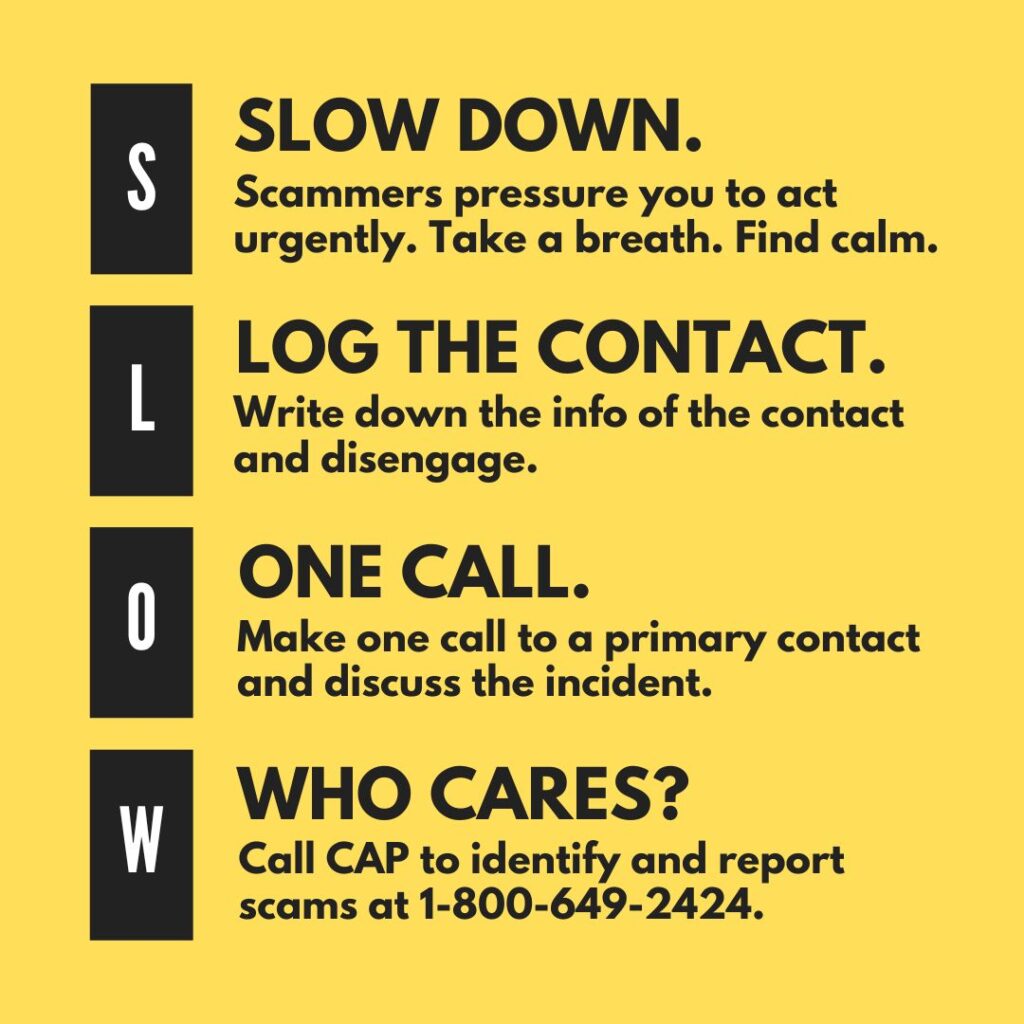

For this scam and consumer transactions generally, you can apply the SLOW method to disrupt the unpredictable reaction response by substituting a planned response instead. At the onset of the first communication, start with SLOW as a strategy to help you take steps to verify.

S – Slow down – scammers pressure you to react urgently. Don’t! Instead, take a breath and find your calm by doing what is immediately natural to you.

L – Log the contact – write down the information of the email, or phone call. If they are on the phone, you can tell them you will call them back, even if you don’t intend to. Then, disengage.

O – One call – make one call to a primary contact, such as a friend or family member and discuss the incident. It works best if you have pre-established who this will be; someone you can trust no matter what. The contact is a sounding board, who will ask questions and help you get curious about the interaction. Some questions might include:

How do I know the contact is who they say they are? –What proof is there? Where can I verify their contact information that is not part of the communication I received? –Was my credit card charged? What other parties can I contact that might know more about this? How can I be sure this is not a scam?

W – Who cares? Contact another party or organization in your life who cares. The Consumer Assistance Program (CAP) can help you identify scams and report them: 1-800-649-2424 and ago.vermont.gov/cap

Know what to watch out for in computer tech scams, so you can avoid them:

- Be wary of pop-ups and unexpected emails/phone calls.

- Watch out for security warnings and account renewals.

- Don’t trust contact information, like links, URLs and phone numbers provided in unexpected emails.

- Never click on links or provide remote access to your computer from an unknown email or source.

- If you received an email or pop-up message, you cannot click out of, don’t engage. Instead, shut down, restart, or unplug your device.

- If you get a call from “tech support,” hang up.

- Be careful when searching for tech support online. Some users have been scammed by calling illegitimate phone numbers listed on the internet.

In the age of the internet and free flowing technology scammers hope to capitalize at every turn. You can prevent scams by practicing SLOW in all your consumer transactions now—and commit to being a primary contact for others. Everyone can help stop scams by following a scam prevention plan and sharing scam knowledge with your community.