There are perfect matches online, and there are scammers. How can a person tell the difference when online profiles of scammers can be just as good as, if not better than, profiles of existing people? Scams that prey on trust and deceive through relationships of confidence and romance are among the most heart wrenching. How can you look for love online, while keeping your heart protected?

Armor your heart. Be romance scam smart.

Armor your heart by using verification strategies:

Verify the person’s identity:

Using image search, you can see how frequently a photo occurs elsewhere online and in different profiles

Ask contacts what they think

Ask photo poses with very specific uncommon photos

Video chat on your terms and don’t accept excuses of having slow internet

Armor your heart by knowing the signs of a scammer:

Refuses to provide additional photos

Refusesto chat through webcam

Is difficult to reach by phone, or prohibited from calling

Has excuses as to why you can’t meet

Needs money, or financial support of any nature, including a business venture

Wants to “strengthen the relationship” by sharing personal identifiable information (accounts, passwords, credit cards, and more) or opening lines of credit together

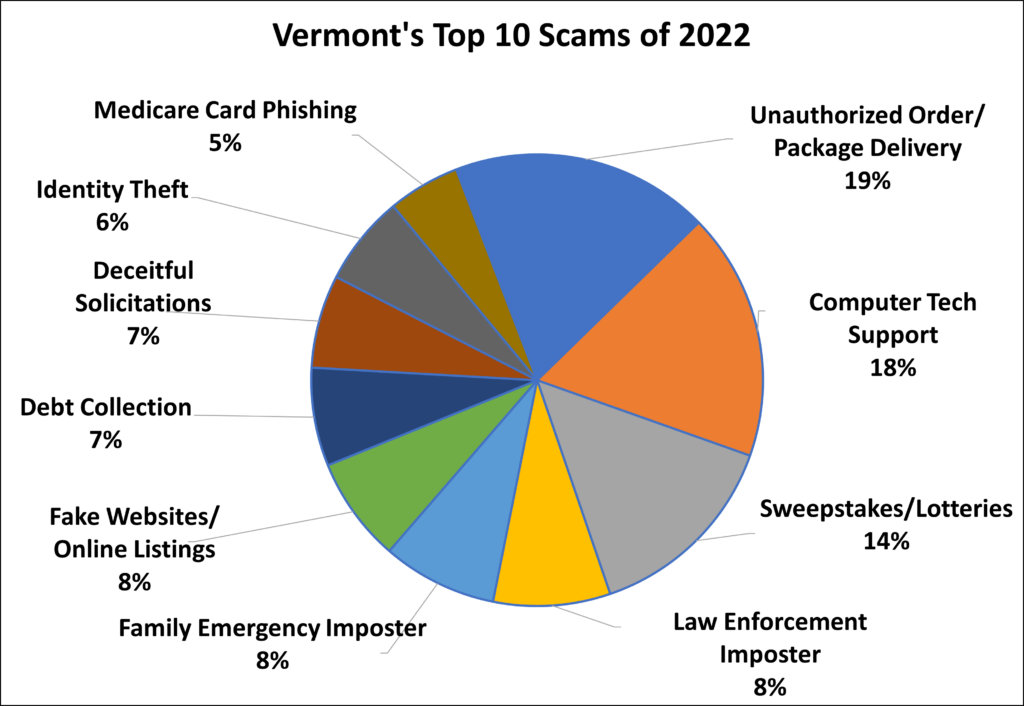

BURLINGTON, VT – Reports of scams to the Attorney General’s Consumer Assistance Program totaled 3,685 in 2022. In keeping with the previous year’s trend, a scam claiming that an unauthorized order was placed, or a package is pending delivery, sometimes naming Amazon, took the number one spot on the list, totaling 19 percent of the top scams reported to the Consumer Assistance Program. Following closely behind in the number two spot was the computer tech support scam, where a scam tech company reaches out about concerning viruses or problems with antivirus services, accounting for 18 percent of the top scam reports in 2022.

Vermont’s Top 10 Scams Reported in 2022 by percentage of the Top 10.

The family emergency imposter scam notably climbed the list from number nine to number five in 2022. Within this category, the grandchild imposter scam, where a grandparent receives a call from a scammer claiming to be a distressed grandchild, resulted in 104 scam reports. In May, the Consumer Assistance Program issued a VT Scam Alert to warn Vermonters about the influx of this scam. Again in June, this category of scam gained attention due to scammers demanding cash be handed over to in-person couriers. In an effort to reduce the impact of this troubling scam, the Consumer Assistance Program produced the Avoiding the Family Emergency Scam video as part of the Imposter Scam Prevention Project education campaign.

The most significant development in 2022’s top 10 list was not the emergence of a new scam, but the disappearance of an old one. For the first time in four years, the Social Security phishing scam fell from the top 10 list. This scam, where you receive a phone call, often a robocall, stating there has been criminal or fraudulent activity involving your Social Security number, accounted for only 2 percent of the top scam reports in 2022. The year prior, it was the second most reported scam.

Potential causes for this drop, and an overall decrease in scam reports by 28 percent in 2022 from the previous year’s 5,154 reported, could be linked to an overall reduction in robocalls coming into Vermont.

YouMail’s Robocall Index shows that robocalls in Vermont deceased by 10 percent, or 5.5 million calls, from 2021 to 2022. At the same time, the Attorney General’s Robocall Enforcement Team targeted the Social Security phishing scam by suing TCA VoIP, a California-based telecommunications company that sent thousands—if not millions—of fraudulent robocalls to Vermont residents. The settlement, finalized in December, required TCA VOIP to close its doors and pay a $37,500 financial penalty.

“Scams affect us all—whether you’ve received an annoying scam call or text, been lied to by a scammer, or lost money to a scam. Together, we can fight scams by reporting them to the Consumer Assistance Program and spreading awareness within our communities. My office helps Vermonters through the Consumer Assistance Program, and we will continue to hold companies that profit from scams accountable,” said Attorney General Charity Clark.

The Consumer Assistance Program actively updates scam prevention resources and strategies and manages the CAP Connection blog, keeping Vermonters informed about important consumer issues.

The scam: You receive an automated phone call, text message, or email claiming that you have been charged for an online order, have an outstanding balance on your account, or are sent an item you did not order. The scammer then instructs you to call a number provided in the scammer’s communications to get a refund or to resolve the charge. At this point, they will ask you to provide your card number to “confirm your account” or prompt you to provide them remote access to your computer. As soon as the scammer has remote access to your device, they can access every single document, file, and transaction you have saved to your device.

How to spot the scam: Companies will not call with tech support unless you requested that they contact you. If you receive a package that you do not recall ordering, check your statement history to see if you have been charged. Packages without a return address are highly suspicious.

What to do: Hang up the phone immediately and do not call back. If you receive an email or text regarding a package delivery or order that has been made, do not click on any links. Mark the email as “Junk” or “Spam”. Furthermore, never allow remote access to your devices to unknown parties. If you are concerned about charges made to your accounts, log in to your account directly and contact your financial institution. If you receive a package that you did not order, mark it return to sender and give it back to the mail carrier.

The scam: You receive a phone call, pop-up, or email on your computer claiming to be from Norton, Microsoft, Apple, or another well-known tech company. They will make claims such as your electronic device has a virus; your device security subscription has been automatically renewed; or state you have been charged for services you did not receive or ask for. You may be prompted to click a link or call a number to contact. They will try to persuade you to give remote access to your device to fix the issue, and sometimes will even ask for immediate payment for their services.

How to spot the scam: Legitimate tech support companies do not display communications to their customers as random pop-ups on your device. Tech support will not call you to warn of security incidents, that your account has been renewed for a subscription you do not recognize, and will not send you random links, often shortened, with instructions for you to click on URLs.

What to do: When contacted about a supposed business relationship, take steps to verify, especially if you do not remember signing up for services. Never click on links or provide remote access to your computer from an unknown email sender or pop-up message on your device’s screen. If you received a pop-up message you cannot click out of, shut down, restart, or unplug your device. If you get a call from “tech support”, hang up. Also, be careful when searching for tech support online. Some users have been scammed by calling inaccurate phone numbers listed online.

The scam: You will be notified by phone, email, or mail that you won a prize or a quantity of money. In some cases, you will even receive a realistic-looking check – but it is fake! You are instructed to pay fees and give your financial and personal information to claim your prize. They often use a legitimate sweepstakes name, like Publishers Clearing House.

How to spot the scam: Legitimate sweepstakes and contest businesses, like Publishers Clearing House and Mega Millions lottery, will contact you in person if you win a major prize. For prizes under $10,000, the notification is done through certified mail by overnight delivery services (FedEx, UPS). They will not contact you by phone, nor require a payment or processing fee to release your prize.

What to do: If it sounds too good to be true, then it’s not true. You don’t need to pay fees or give your financial information in order to claim a prize.

Law Enforcement Imposter

The scam: You receive a phone call unexpectedly, claiming to be a police officer, U.S. Marshall, or U.S. Customs and Border Protection. The caller threatens arrest or legal action. When you engage, urgent payment is demanded to make the problem go away. Payment does not solve the supposed problem, and they keep calling.

How to spot the scam: The police would not warn you ahead of time about a pending warrant or arrest. Using such threatening tactics intend to spike your emotional response.

What to do: Hang up on all arrest threats and report them. Watch out for similar government imposter scams that purport to be agents of government, including from the Social Security Administration, the Department for Children and Families, the IRS and more.

The scam: Scammers pose to be someone you trust and pretend to be in an emergency to convince you to send them money or will ask you for a favor. These scammers pose as grandchildren, friends, relatives, and close contacts appearing to be someone you know. Scammers impersonate people you love and play on your fears to have you send money urgently. After the initial call, you may be told a lawyer, parole officer or courtroom may contact you for further information.

How to spot the scam: Contacts come in as calls, emails, or online messages. Sometimes it’s someone you haven’t heard from in a while. They require urgency and ask for secrecy. You may be instructed not to speak to your loved one on the phone.

What to do: Take steps to verify. Check out if they really are who they say, even if they sound like a loved one. Slow down your response and contact someone you trust to verify if there is an emergency. You can also choose a “code word” with friends and family to verify the person is who they claim to be. If they don’t know the word, they are not your friend or family member.

The scam: Fake websites or phony listings draw you into a purchase that’s likely too good to be true. Listings may include Facebook Marketplace and Craigslist posts that don’t deliver after payment has been made, cheap pet sales, and websites with steep discounts. This scam can also appear in online rental listings as well as target online sellers.

How to spot the scam: Be skeptical of unrealistic offers. Watch out for requests for money in any form (gift cards, wire transfers, cash) when not made in person. Scammers likely will not want to talk on the phone or meet in person. Heed warnings in user reviews and other online commentary.

What to do: Investigate the person/profile of the seller. If their profile is new and they have no friends and photos, they are likely a scam. Research new websites you are considering doing business with by looking up online reviews and state business registrations, taking note of how long the company has been operating. Perform online searches of the business with “scam” and “complaints” to see if issues generate. Complete your transactions in cash and preferably a safe place in-person.

Debt Collection

The scam: Scammers pose as debt collectors and require immediate payment. They may claim to be familiar businesses and threaten utility disconnection or legal action.

How to spot the scam: Collectors are not allowed to threaten you with arrest over debts owed. You can request verification of the debt, which must be sent to you in writing. If you ask them to stop calling you, they are generally required to stop.

What to do: Hang up the phone, and if they call again, let the call go to voicemail. If you think you do actually owe money to a debt collector or other agency, make sure to use trusted contact information when communicating with them. You can also contact the originator of the debt to see if they sold the debt to a debt collection agency, and request they provide you with the name of the debt collector who took on the debt.

Deceitful Solicitations

The scam: You receive unsolicited communication with a deceptive promotion. Offers may appear to be from a known business, like Xfinity or DirecTV, and extend unreal offers. Solicitations may purport affiliation with a charitable cause or make low-ball offers on the sale of real estate, urging recipients to complete an enclosed one-page form contract to sign over their home.

How to spot the scam: Beware of unsolicited offers you cannot verify. Be especially weary of offers that ask you to complete the transaction in one sitting.

What to do: Hang up on unknown callers and let calls go to voicemail. When you receive mailings, take extra time to reply by inspecting the details and using your personal contacts as a sounding board. Never give over your payment information or sign on the line when you don’t understand the offer or details.

The scam: Your personal information is compromised and used for another’s financial gain. This can look like receiving a letter about a new account opening, or the discontinuance of bills. You might stop receiving legitimate bills and other mail or start to get bills for products and services that you didn’t arrange.

How to spot the scam: Beware of communications denoting unexpected bank transactions, credit card or benefit applications. If your expected bills are not showing up, or you are receiving correspondence in someone else’s name, report it.

What to do: Don’t give out personal information, such as your Social Security number, passwords, personal identification numbers, and financial accounts. Review your credit reports at least once a year. (You can access your credit report for free). Carefully check bank account statements and benefits to verify transactions. Shred documents and expired credit cards before you throw them out. Verify security breach notification letters received on the Attorney General’s website. If your information has been stolen by an identity thief, take identity theft protection steps.

The scam: Scammers will call, often with a live call and from a spoofed caller ID number, and pose as Medicare representatives to gain your personal information and money. These scams are most frequent during times of open enrollment but can occur year-round. The scammers will state they need your Medicare card number or Social Security number to keep your coverage active and verify medical information. The calls may also claim that coverage is expiring or in need of renewal. Scammers will also ask if you received a “new Medicare card.”

How to spot the scam: In general, Medicare cards do not expire. Unless you have called Medicare using the 800 number on the back of your card and requested a callback, Medicare will not call you. If a phone call is required, you would receive a letter from the Social Security Administration to schedule a call. Medicare representatives will never call you in an attempt to verify your information, sell you products, tell you that your coverage is expiring, or to issue you a new card.

What to do: Never provide your Medicare number or other personal information and payment to unknown callers. In Vermont, representatives of the State Health Insurance Assistance Program (SHIP) at 1-800-642-5119 through local Area Agencies on Aging can help address Medicare questions. Other questions and concerns about Medicare coverage can be directed to Medicare at 1-800-MEDICARE.

It happened last year, and again this year. During Medicare Open Enrollment season, a concerned elder in my life called to ask if the person soliciting them was a scammer or an actual enrollment representative. The truth is, aside from highlighting some key identifiers of scams, it can be hard to tell. The scammers are so good at acting as if they are Medicare enrollment professionals, that it is enormously difficult to differentiate them from the real deal. The scams even spoof Medicare’s phone number, making the caller ID appear to be Medicare when it is not.

Medicare Open Enrollment Scam Alert

The primary difference between a telemarketer and a scammer is whether the caller is honoring the Federal Do Not Call Registry (DNC). If you ever put you number on the DNC by calling 1-888-382-1222 or by going online at donotcall.gov, you should not be receiving calls from solicitors—Even during Medicare open enrollment. You likely should not be receiving robocalls of this nature either.

What provider can call you when you are on the DNC?

Businesses with whom you have a customer relationship within the past six months, such as your Medicare provider, and other you have requested to call you. Yes, that’s it. No other unrequested calls are allowed.

The same goes for those annoying automated/computer/robot calls. Except with these, unless you expressly opted into receiving robocalls in writing, you should not be receiving these calls either.

What if the call IS my Medicare provider, or I am interested in changing plans during open enrollment?

This is where it gets tricky. It is difficult to know whether your provider is calling instead of a scammer, especially because scammers copycat caller ID numbers. The only way to be sure is to take steps to verify by hanging up on the caller and calling back a number you know to be valid.

If you are looking to change enrollment during the Medicare open enrollment period, do so on your terms.

If you are concerned about your Medicare plan or need to report known Medicare provider fraud/abuse, contact Medicare directly at 1-800-MEDICARE (1-800-633-4227).

Please help the Consumer Assistance Program (CAP) stop Medicare scams by sharing this information with someone you know. If you have questions about this scam, or have provided personal information to the scammers, please contact CAP at 1-800-649-2424 or go online to ago.vermont.gov/cap.

It is not every day that government relief is offered for paying off student loans. In the past, to help warn about scams, I can recall specifically saying something to the effect of, “The government doesn’t give you money to pay for your student loans.” Now that the government is, in fact, giving certain qualified borrowers some student loan debt relief (studentaid.gov), my blanket statement no longer applies. Criminal fraudsters may take advantage of this rare opportunity by representing themselves as providing this student loan debt relief.

To make sure you are connected to the most accurate information when claiming your portion of the student loan forgiveness, connect with known legitimate sources.

The Federal Department of Education set up a “Federal Student Loan Borrower Updates” subscription so that you can receive notifications: https://www.ed.gov/subscriptions

Want to connect with someone locally? Vermont’s own VSAC has a wealth of information about student aid and stays in the know about available government programs.

Reach out to your loan servicer and update your contact information. Get your loan servicer information from your StudentAid.gov account.

Keys to detecting a student loan relief scam:

You never need to pay to claim your federal loan forgiveness. Hang up on calls asking you to pay!

The government does not solicit your participation in student loan relief programs, so you should not receive calls about it or click on ads offering student debt relief.

Hang up on callers asking for your Federal Student Aid/FSA ID. The Department of Education and your federal student loan servicer will not contact you to ask for this information. Keep your information safe from identity thieves, who may try to claim your student loan relief for themselves!

Companies offering debt relief in Vermont are required to be a licensed debt adjuster with the Vermont Department of Financial Regulation (DFR) Division of Banking. If you are interested in consolidating student loans, make sure the business meets the licensing requirements of our state and verify this with DFR.

Have you been contacted by student loan debt relief scam? Help others by reporting it!

Our nation’s consumer protection agencies, the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) are working together to hold scammers accountable. “Over the course of the last 18 months, the FTC has reached nearly $30 million in settlements that included refunds for tens of thousands of student borrowers who were illegally charged up front fees and falsely promised reduced or eliminated student loan payments” (whitehouse.gov). Since 2011, the CFPB has required “refunds of nearly $8.7 million to consumers and banning several individuals from the debt-relief payment processing industry…” (whitehouse.gov)

Report scams directly to the Federal Trade Commission: reportfraud.ftc.gov

Report scam calls to help the Federal Communications Commission (FCC) identify scam callers. Send your Student Loan Scam report to StudentLoanScams@fcc.gov and include the date of the call, time of the call, the recipient’s phone number, the number on the caller ID.

The Consumer Assistance Program is your state resource to help identify and report scams. File with CAP through our online scam form or call us at 1-800-649-2424.

This weekend, I am going to a Shred Event hosted by a local bank. My several boxes of shred-necessary paperwork–you know the documents riddled with personal identifying numbers–already seem lighter.

Banks periodically host events where they gather one or more mobile shred trucks, equipped with an industrial shredder and invite the public to offload their shredding. Different from an at-home shredder, which slowly snips small amounts of paper at once with varying outputs, cutting long strips or crosswise. The shredder on a mobile shred truck can handle large quantities of paper. An entire box, for example, can be dumped into the receptacle at once, returning small bits of paper. In the world of paper shredding, industrial shredders are considered quick and supreme. The result of compounding shredders with the anonymity of event participants is a massive indiscernible pile of recyclable paper.

Shred Events: Protect Your Identity

Why shred events?

Shred events help prevent fraud and financial identity theft by giving people an easy way to dispose of confidential paperwork. We all have it, and we need a safe and secure way to dispose of it. All an identity thief needs to wreak havoc on our financial future is our Social Security number, date of birth, address, and name. Shred events benefit you by helping you protect your personal information. They help banks by way of protecting the information of their clientele and eliminating potential bank fraud and related recovery costs.

Identity thieves are online, so why do we need to shred paper?

News of data breaches and the message to stay safe online and protect your electronic information remains true and important. And still, some of the more involved and impactful crimes of identity theft, such as the creation of new accounts and huge losses, are often committed by people close to us: a relative, supposed friend, or neighbor. Some of these folks may know exactly where you keep your boxes of personal files.

Still others may forage trash the eve of trash pickup. If you carelessly discard confidential documentation, you could be directly supplying a thief with your information.

Destroying documents that you no longer need is the best method to prevent potential theft and misuse of that document. Keeping such documents around your home, or neglectfully discarding them in original form makes you more susceptible to identity theft.

Can shred events destroy my devices that contain my personal information?

No. Shred events are all about shredding paper. Personal devices cannot be discarded or wiped clean of personal data there. Prior to discarding or recycling electronic devices, consumers must take crucial steps to clear personal data off a device through a factory reset or destroy the dive/circuit board altogether.

How can I find a shred event near me?

Banks as well as community organizations host shred events. When you find an event, such as through an online event listing on a third-party site, like Facebook, take steps to verify directly with the hosting entity.

To learn more about identity theft and protection steps, please review the Consumer Assistance Program’s website and blog.