By Crystal Baldwin

This time last year, I had no idea my whole life would be online—work, exercise, shopping excursions, and more. Now that pretty much every facet of my life, and likely yours too, involves the internet, we must be on the lookout for new and developing scams to prevent ourselves and our friends and loved ones from being scammed.

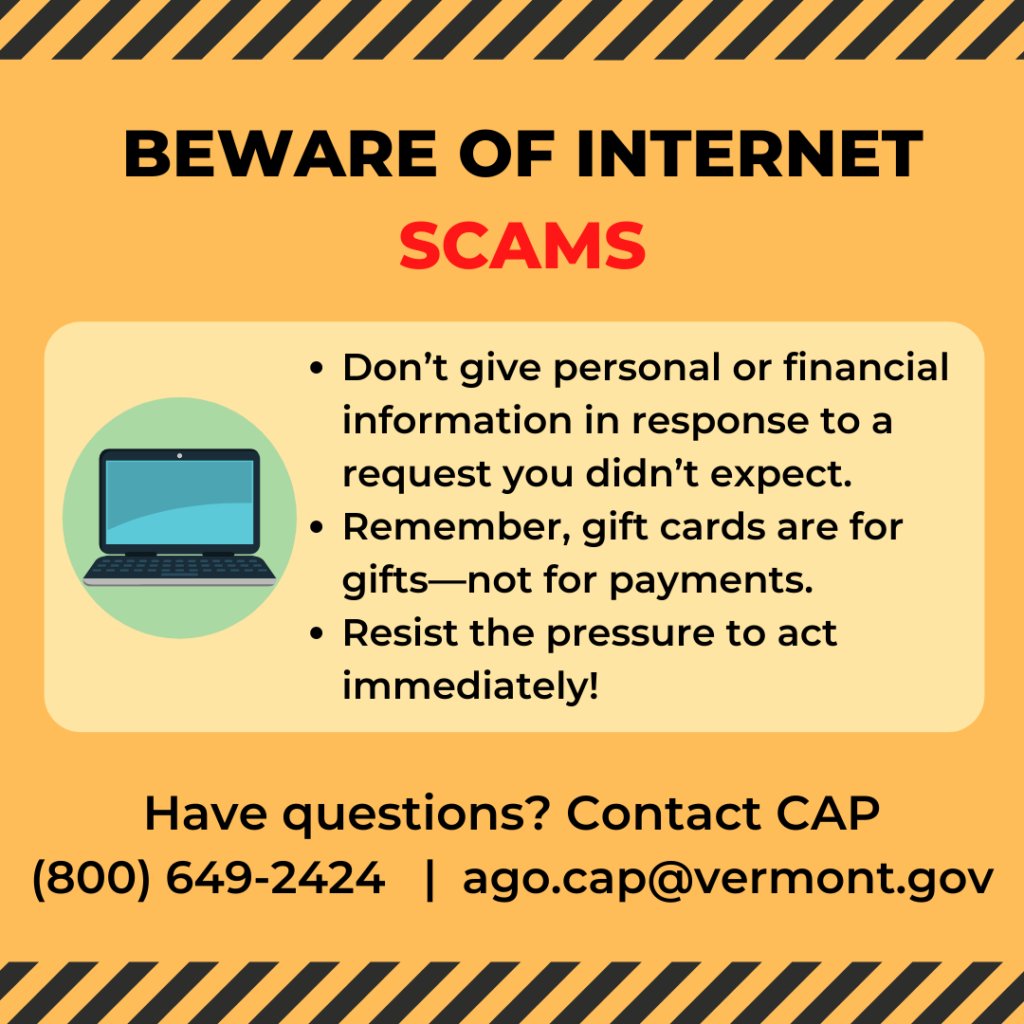

Common scam signs are unverified requests for personal information and money, whether requested through gift card, wire transfer, cash, peer-to-peer payment, postal money order, or check.

The following are some anticipated internet scams to avoid:

CEO/boss and business/organization personnel imposter scams: Business personnel working remotely, in distracting environments and away from regular exchange with colleagues, may receive urgent messages from someone purporting to be their boss or colleague ordering funds to be transferred.

- Spot the Scam: Scammers create an email address like your colleague’s and assign the name of the email account holder to be the person’s name.

- How they trick us: It is easy to miss that the details of the email address have changed, particularly when operating on mobile devices, which often only display the email sender’s name.

- Scam Prevention: In business operations, put into place verification checks. Ensure one check includes verifying requests directly with the sender through a phone call or video chat. Also, require a third party to be involved, such as another colleague

Job and work-at-home offers and business opportunity scams: These involve enticing offers to make a lot of money in exchange for performing simple tasks and transmitting money.

- Spot the Scam: Commonalities among all such scams offer work that is too good to be true, ask for payment or your personal information at some point, and refuse to communicate with you by video chat on your terms.

- How they trick us: These scams can hide in plain sight, often posting in known online listings, like LinkedIn and Indeed, and even post listings under known business names.

- Scam Prevention: Standard application and onboarding procedures apply to home-based jobs as onsite positions: You never provide your personal information up front. You never have to give money to your employer. For business opportunities, the FTC prohibits the exchange of payment prior to the issuance of very specific disclosures.

Friend-in-need and fake crowdfunding scams: We have heard reports of Vermonters responding to emailed and messaged requests for help for various needs, such as to support missions and charitable causes, some scammers even claim to be the pastor of a congregation. The scam pulls us in as we strive for connection and community through this time of isolation. We want to be helpful but can’t volunteer in the personal ways we used.

- Spot the Scam: The message comes as a surprise and you can’t reach your friend through other methods, such as by phone, except the digital way in which you received the message.

- How they trick us: We are convinced that the communication is actually coming from our friend and we do not know that their account was likely hacked or a fake account was created to solicit you.

- Scam Prevention: Take steps to verify, even if the solicitor requests you not to tell others. A phone call to the person directly or another who is aware of the person’s whereabouts is key here.

Fake news and affiliated endorsement of cure-all products: Scammers will take advantage of consumers accessing news online and claim to have exclusive cures and vaccines.

- Spot the Scam: The news popped up in a social media feed, in an email, or in a news alert with a media name you did not recognize. The information is not verified in other reputable news sources, or through a known health organization.

- How they trick us: The alerts and ads use compelling stories and scare tactics that trigger us to respond emotionally, rather than rationally, to false promises.

- Scam Prevention: Regularly check-in with trusted websites, such as the CDC and Vermont Department of Health for updates on the status of the virus and how it is being treated.

Fake charities: As is common with disaster and crisis scams, consumers can expect fake charity scams to prey on their generosity to help others in need. They will most definitely occur online but may also occur by phone.

- Spot the Scam: Unsolicited requests for donations by a charity you have never heard of and cannot verify.

- How they trick us: They take advantage of our desire to help others and the sense of urgency to respond.

- Scam Prevention: Verify the charity by using websites like Charity Navigator and the BBB’s Giving Wise Alliance. Always request solicitations in written form to give you time to do your research and consider the ask. Give to known charities and assign designation to specific causes.

This is not a comprehensive list of the scams that may be encountered online. New scams will develop, and when they do, we ask that you share the information with your community as well as with the Consumer Assistance Program at ago.cap@vermont.gov .

Help us stop these scams by sharing this information with those you care about. Get notified about the latest scams: Sign up for VT Scam Alert System alerts.