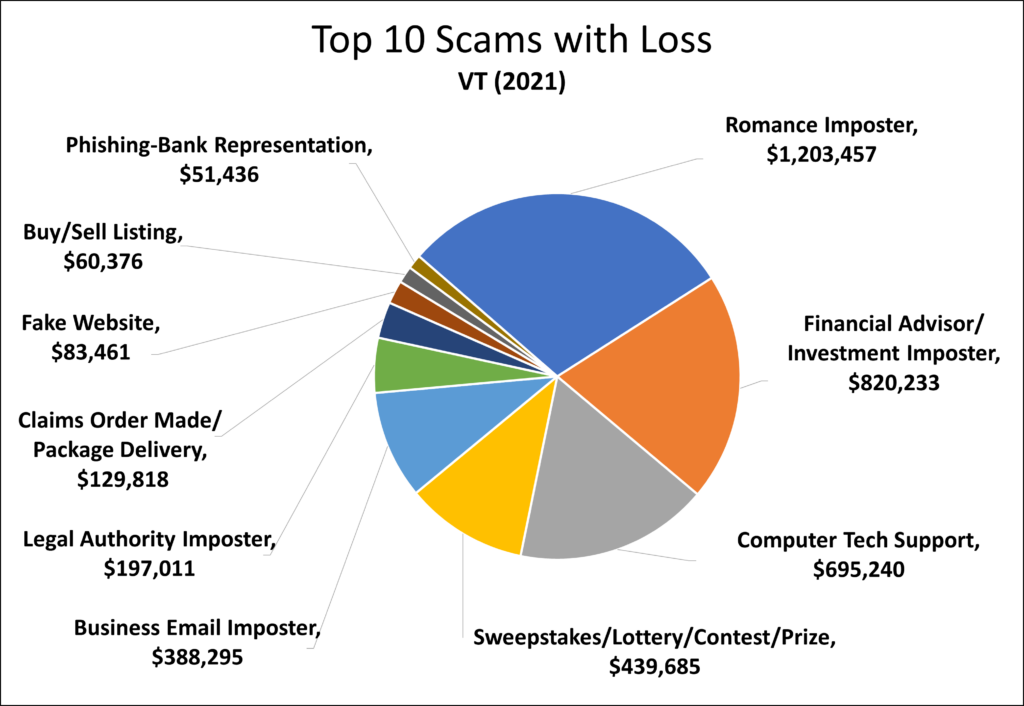

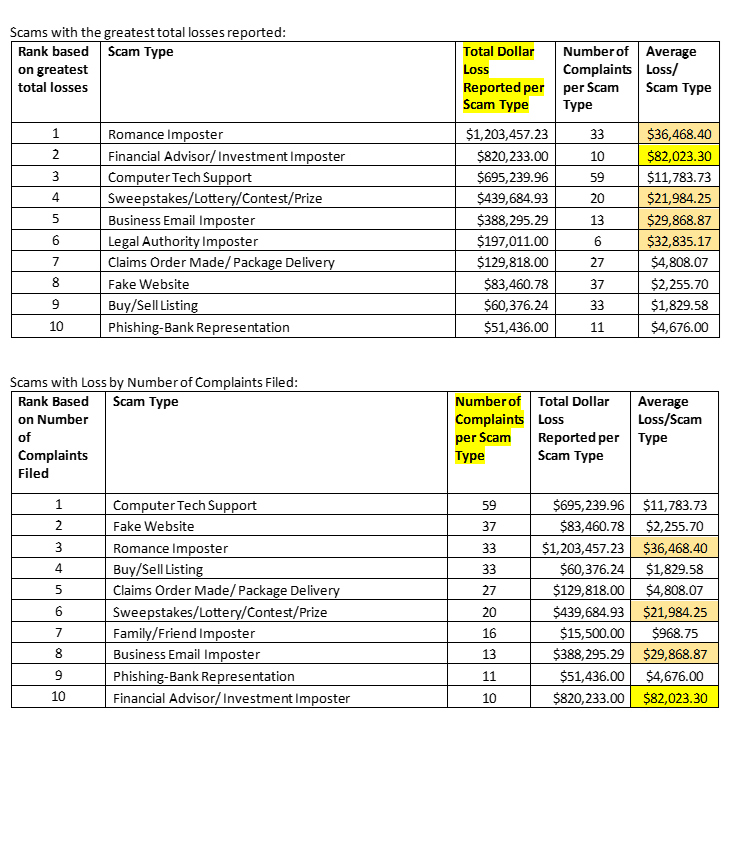

Reports of scams to the Attorney General’s Consumer Assistance Program (CAP) totaled 5,154 in 2021, up just slightly from the previous year’s 5,021 reports. As imposter scams are of ongoing concern in Vermont, CAP recently distributed a video imposter scam prevention project, highlighting three concerning imposter scams with high dollar loss: the Romance Imposter scam, the Family Emergency/Imposter Scam, and the Business Imposter Email Scam. We work in partnership with the Community of Vermont Elders (COVE), FAST of Vermont and local community partners to provide referrals and resources to victims of scams. In addition, CAP connects with service providers and local community organizations to provide training and scam prevention presentations.

As highlighted in the prevention project, taking steps to verify can help individuals avoid scams. A simple verification process to follow for all scams is the SLOW Method:

S – SLOW DOWN

Scammers pressure you to act urgently. Don’t!

L – LOG THE CONTACT

Write down the info of the contact and disengage.

O – ONE CALL

Make one call to a primary contact and discuss the incident.

W – WHO CARES?

Call CAP to identify and report scams at 1-800-649-2424.

CAP reminds Vermonters to never give out personal information or make payments to parties you cannot verify. Scammers will ask for payment in all forms, including wire transfer, cryptocurrency, cash, peer-to-peer payment, money order, check, credit/debit card, and gift cards. If you have sent money to a scammer, follow recovery steps now.

Vermonters can help stop scams by sharing information with community members and by reporting scams to CAP to support educational outreach. To report scams, complete CAP’s online scam reporting form or call 1-800-649-2424.

Computer Tech Support (Traditional)

The scam: You receive a phone call, pop-up, or email on your computer claiming to be from Norton, Microsoft, Apple, or another well-known tech company. They will make claims such as your electronic device has a virus, your device security subscription has been automatically renewed, or stating you have been charged for services you did not receive or ask for. You may be prompted to click a link or call a number to contact. They will try to persuade you to give remote access to your device to fix the issue, and sometimes will even ask for immediate payment for their services.

How to spot the scam: Legitimate tech support companies do not display communications to their customers as random pop-ups on your device. Tech support will not call you to warn of security incidents; that your account has been renewed for a subscription you do not recognize; and will not send you random links, often shortened, with instructions for you to click on URLs.

What to do: When contacted about a supposed business relationship, take steps to verify, especially if you do not remember signing up for services. Never click on links or provide remote access to your computer from an unknown email sender or pop-up message on your device’s screen. If you received a pop-up message you cannot click out of, shut down, restart, or unplug your device. If you get a call from “tech support”, hang up. Also, be careful when searching for tech support online. Some users have been scammed by calling illegitimate phone numbers listed on the internet.

Fake Website/Online Listings

The scam: Fake websites or phony listings on sites like Facebook Marketplace and Craigslist draw you into a purchase that’s likely too good to be true. This scam can also appear in online rental listings, and as a buyer offering well-over the selling price for an item. As a seller, the fake buyer sends a fake check or pays with a fraudulent credit card and asks you to advance funds to another fake vendor, causing you to be out the funds.

How to spot the scam: Be skeptical of unrealistic offers. Watch out for requests for money in any form (gift cards, wire transfers, cash) when not made in person. Scammers likely will not want to talk on the phone or meet in person. Heed warnings in user reviews and other online commentary.

What to do: Playing it safe online takes a bit of detective work to determine legitimacy of an offer. Investigate the person/profile of the seller. If their profile is new and they have no friends and photos, they are likely a scam. Research new websites you are considering doing business with by looking up online reviews and state business registrations, taking note of how long the company has been operating. Perform online searches of the business with “scam” and “complaints” to see if issues generate. Complete your transactions in cash and preferably a safe place in-person.

Romance Imposter

The Scam: Scammers connect usually through social media and pose to be someone you trust and care for. After the trust has been developed, they claim they are in an emergency to convince you to send them money or will ask you for a favor. Scammers impersonate a love interest and play on your fears to have you send money urgently.

How to spot the scam: Use reverse image searches to look up images of the person; if ther are many results, the contact may be using someone else’s image and is a scam. Video chat on your terms and at random times. If they are typically unavailable, they may be scamming someone else.

What to do: consult with your close in person contacts and reach out to an organization in your life who cares. They may spot something you don’t. Never send money to someone you have not met in person.

Computer Tech Support (Claims Order Made/Package Delivery)

The scam: A variation of the traditional Computer Tech Support scam (see # 3 below). You receive an automated phone call, text message, or email claiming that you have been charged for an online order, have an outstanding balance on your account, or are sent an item you did not order. The scammer then instructs individuals to call a number provided in the scammer’s communications to get a refund or to resolve the charge. At this point, they will ask you to provide your card number to “confirm your account” or prompt you to provide them remote access to your computer. As soon as the scammer has remote access to your device, they can access every single document, file, and transaction you have saved to your device.

How to spot the scam: Companies will not call with tech support unless you requested that they contact you. If you receive a package that you do not recall ordering, check your statement history to see if you have been charged. Packages without a return address are highly suspicious.

What to do: Hang up the phone immediately and do not call back. If you receive an email or text regarding a package delivery or order that has been made, do not click on any links. Mark the email as “Junk” or “Spam”. Furthermore, never allow remote access to your device to unknown parties. If you are concerned about charges made to your accounts, log in to your account directly and contact your financial institution. If you receive a package that you did not order, mark it return to sender and give it back to the mail carrier.

Sweepstakes/Lotteries/Contest/Prize

The scam: You will be notified by phone, email, or mail that you won a prize or a quantity of money. In some cases, you will even receive a realistic-looking check – but it is fake! You are instructed to pay fees and give your financial and personal information to claim your prize. They often use a legitimate sweepstakes name, like Publishers Clearing House.

How to spot the scam: Legitimate sweepstakes and contest businesses, like Publishers Clearing House and Mega Millions lottery, will contact you in person if you win a major prize. For prizes under $10,000, the notification is done through certified mail by overnight delivery services (FedEx, UPS). They will not contact you by phone, nor require a payment or processing fee to release your prize.

What to do: If it sounds too good to be true, then it’s not true. You don’t need to pay fees or give your financial information in order to claim a prize.

Family/Friend Emergency/Imposter

The scam: Scammers pose to be someone you trust and pretend to be in an emergency to convince you to send them money or will ask you for a favor. These scammers pose as grandchildren, friends, relatives, and close contacts and seem like the real deal. Scammers impersonate people you love and play on your fears to have you send money urgently. After the initial call, you may be told a lawyer, parole officer or courtroom may contact you for further information.

How to spot the scam: Contacts come in as calls or emails or online messages. Sometimes it’s someone you haven’t heard from in a while. They require urgency and ask for secrecy. You may not be allowed to speak to your loved one on the phone.

What to do: Take steps to verify. Check out if they really are who they say even if they sound like a loved one. Slow down your response and contact someone you trust to verify if there is an emergency. You can also choose a “code word” with friends and family to verify the person is who they claim to be. If they don’t know the word, they are not your friend or family member.

Phishing-Bank Representation

The scam: You receive an email or phone call claiming to be from a bank. Emails might claim that your account is in danger or has been suspended, or that your card is on hold due to suspicious activity. The email also includes links to phony websites. Phone calls may claim that there has been fraudulent activity involving your account, and the scammers demand personal information about you and your account.

How to spot the scam: Scammers mask their actual identity by changing the sender name to the name of the financial institution. Look at the email address before opening the email. You will often find an account not affiliated with your bank. Similarly, scammers can spoof phone numbers of financial institutions. If you answer a call that appears to be from your bank and they ask for your personal and/or account information, hang up and call your bank directly on a number you trust to verify their attempt to contact you.

What to do: Do not reply to the email or click on any links or attachments included in the message. If you receive a call, hang up the phone. To correspond directly with your bank or financial institution, use verified contact information, such as information listed on your statement.

Financial Advisor/ Investment Imposter

The scam: Scammers are spoofing websites and using fake social media accounts to obscure their identities. Scammers also pose an imposter friend with an investment tip. Investors should always take steps to identify phony accounts by looking closely at content, analyzing dates of inception and considering the quality of engagement. To ensure investors do not accidently deal with an imposter firm, pay careful attention to domain names and learn more about how to protect your online accounts.

How to spot the scam: Beware of fake client reviews. Scammers often reference or publish positive, yet bogus testimonials purportedly drafted by satisfied customers. These testimonials create the appearance the promoter is reliable – he or she has already earned significant profits in the past, and new investors can reap the same financial benefits as prior investors.

What to do: The North American Securities Administrators Association (NASAA) recommends investors independently research registration of investment firms.